Hello, I’m back on this blog. I still do visit my blog and pay for my domain but time has been robbed of me that I find it so difficult to make time to commit to writing here. But there have been a few topics I have been feeling very strongly about and they range from grief to finance – winning combination, and since I am planning on hopping on a new finance adventure (I promise to write about it once we’ve begun and made some progress) – I thought I will share some insight on how I have managed to build a habit out of saving.

I am also hoping (and maybe even praying) that my cough journey’ cough into writing about personal finance is helpful to open up this discussion that is considered taboo, as to how sex is. Also, women talking about finance? I can count the number of eyeballs that are stuck in the back of people’s heads. However, if this isn’t for you, no one is asking you to read this. I am writing this only because a lot of the content that I have read, watched or listened to on personal finance comes from the West and more often than not, from men.

Which is fine.

I will take any knowledge that is made available to me. But I would prefer to have access to personal finance content that doesn’t talk about a 401k or a Roth IRA. I want to talk about EPFs, investing in gold like our grandparents did and FIXED (not term) deposits. I want to hear language that is familiar to me from people I can relate to. Maybe, I’ve been on the wrong side of the internet that my algorithm is tuned to the Americas. But as I’ve seen the void in this space of South Asian women talking about personal finance, I would like to talk about it, using a platform that is available to me. Also, I know that talking about personal finance isn’t correct, but I have trouble falling asleep at night sometimes, so bear with me.

Now that my justifications are done (I know I should stop someday doing that) let’s talk about how I managed to become consistent with my savings.

Also, I know that I already did my justification, (lol) but I have to add this extra justification in. I am aware that I am of a privileged status to be able to save. I have access to many ‘luxuries’ and conveniences many others may not. So I won’t say that the following would be for everybody. It would probably narrow the scope of this article, but this is probably for someone who lives in an urban setup and who is of the middle class or above. There are many realities I have not seen myself, so this is not a generic article encouraging anyone and everyone to save.

Also, I currently don’t have any credit cards – not really something I consciously do, but I’ve seen the downside of credit card debt in my immediate family so it’s safe to say that I’m still traumatised.

And finally, I am not a financial expert.

If you don’t already, make a budget, preferably, before you get paid

Now, I started saving consistently only in my late 20s. However, I have been making a budget, since forever it seems. Whether I stuck to it or not is a different question. If you have a monthly salary that comes into your account, this is pretty straightforward. However, if you work a few jobs and have multiple salaries coming in, write them down also with a rough indication of the dates the money should come to you.

When making a budget your would first reduce your priority payments and then the bulk of any discretionary spending. Now priorities may mean different things to people, however, I personally believe that if you want to cultivate a saving habit, these should more or less look the same.

To make things easier, here is a look at my current list of items I put in monthly budget:

Priority items

- Savings

- Money for extended family

- Education

- Bills

- Groceries and household expenses

Discretionary

- Salon

- Since it’s a pandemic I don’t really go out, so this would sometimes mean a game on Origin, alcohol for home consumption, some skincare, gifts for family and/or friends or shopping. But it’s very infrequent.

Consider savings as an expense

This was one of the best pieces of advice I had heard from many of the personal finance content I have consumed over the year. Treating savings as an expense is a real game-changer. It sounds a bit bizarre at times, but the best way to do it is to have a standing order to ensure that a certain amount is credited to your savings account every month. I personally don’t have a standing order – I’ve always treated savings as an expense, even when I had my car and had to make the lease payment on that, I would make sure that it’s paid before the due date. I feel the same way about savings and ensure that it’s one of the first things I transfer out of my checking account (your main transactional account).

And what’s a good amount to save? I think experts say 20% of your salary by honestly, if you have never saved before, that can be overwhelming. I would say a mandatory 10% to start with and we take it from there. The important goal behind building a habit of saving is to ensure you save consistent no matter how small it is. It’s more important that you save 10% every month as opposed to 40% every whenever you feel like you are able to.

Also, side note – I think the narrative around personal finance has changed so very much. From our parents time to maintaining a balance on a credit card to our generation paying it off in full. I don’t have a credit card of my own so I don’t know where I stand on this. Similarly, with savings, I think starting small and being consistent even if it’s LKR 5,000 a month x 12 months, is still a good habit as opposed to LKR 15,000 x 05 times a year. While the latter will add up to a larger number at the end of the year, it doesn’t really instil a habit in you and savings from what I have learnt, comes down to building that habit.

Have a separate account for your savings

Now, this is probably what was most infuriated about when it came to the local context after consuming all of that personal finance content. We don’t have a lot of high-yield savings accounts for those who are starting out. Even the ones that are there have a minimum balance requirement of at least LKR 50,000, which isn’t ideal for someone who is starting out to save.

In fact, with my time spent in banks these past two years, I think banks here in Sri Lanka make it so difficult to instil in people a habit and encourage them to save. They waste so much of your time that you would think they don’t want your money.

Now for a separate savings account – I did go the hard route. While I was sure to put aside the required amount of money every month without a standing order, I wasn’t certain if I could trust myself to not pull out the money. So, I opened an account in a whole new bank and got only a savings book and SMS banking that told me my bank balance when I deposited. No ATM card, no online banking. The idea is to make sure that it’s out of sight, out of mind. Well in your mind, but difficult to access.

Also another side note – I would encourage all those who have similar accounts to also have nomination forms completed as well in the case of untimely deaths, like what we are seeing now.

So, I bank with Commercial Bank and Sampath Bank and opened my savings account in Bank of Ceylon. Also, if women don’t already know this, there are ‘special’ women’s accounts, which are ridiculous really haha, but they give you a slightly higher interest rate, usually around 0.5 – 1% more than the regular savings accounts. Currently, this is not issued due to the pandemic (sigh) and the rates are as pathetic as the usual savings accounts, but, it’s good to keep in mind.

Track finances

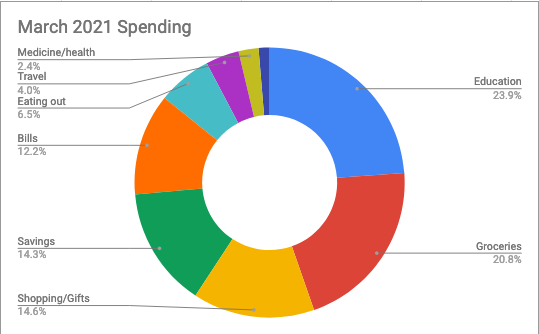

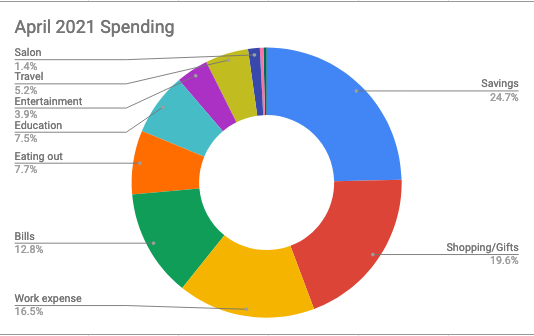

This is cumbersome, but if you’ve never saved, I encourage you to do this at least for three months just so you are able to understand where you are spending the most. There are really great apps out there, I personally like having an excel sheet with the spending and at the end of the month, I tally the credit and debit and that’s okay if it doesn’t match your bank balance or cash at hand. If I’m not lazy I sometimes even try to do a pie chart of the expenses.

For the purpose of this article, I did two pie charts of my spending for March and April 2021. Some of the numbers aren’t ideal but as everyone knows, sometimes you can’t plan or budget for everything. Including funerals and sudden expenses.

There are a few more things I want to talk about, but this is turning out to be a little longer than I had hoped for, so I am going to break this into two parts. The next four steps of sorts are on how you can keep at this habit, now that we have hopefully, put it in place.

Writing about this has been daunting. If you have any feedback or anything at all you would like to add, please do let me know and I would be happy to listen.

#ThinkSunny🌻

PS – It’s crazy to think how my first ‘article’ on this was in 2016. This HAS been a long time coming!

4 thoughts on “How to be Consistent with Savings – I”